Federal Government Releases Further Details Regarding the Proposed Canada Emergency Wage Subsidy

In an effort to preserve Canadian jobs, the federal government has announced the proposed Canada Emergency Wage Subsidy program. The hope is that employers can use this subsidy to keep their current employees and rehire some of those that have been laid off. At the time of writing, this program still requires Parliament’s approval.

What does the program provide?

The Canada Emergency Wage Subsidy will be provided to eligible businesses to subsidize their payroll. The subsidy will apply at a rate of 75% of the first $58,700 normally earned by employees (up to $847 per week). The program will run for 12 weeks, from March 15, 2020 to June 6, 2020. This subsidy applies for existing and new employees.

The amount of the subsidy will be different for each employee. For each particular employee, the subsidy amount will be generally 75% of the amount of remuneration paid to that employee, to a maximum benefit of $847 per week per employee. Employers are not limited on the number of employees that may be subsidized.

If an employer is re-hiring an employee because of the subsidy, employers are expected to pay those employees the same amount they were earning before the crisis. Employers are required to attest that they’re making best efforts to do so.

An employer cannot claim the wage subsidy for an employee for a week that the employee is eligible for the Canadian Emergency Response Benefit.

If an employer is eligible for both the Canada Emergency Wage Subsidy and the temporary 10% wage subsidy (described below), the amount received from the 10% wage subsidy in a specific period will generally reduce the amount available to be claimed under the Canada Emergency Wage Subsidy in that same period.

The wage subsidy received by an employer will be considered government assistance and included in the employer’s taxable income for the year. Assistance under either wage subsidy reduces the amount of remuneration expenses eligible for other federal tax credits calculated on the same remuneration.

Subsidy funds are expected to start flowing to businesses within the next three to six weeks. Employers should register for direct deposit to avoid further delay.

The government will be actively looking for employers abusing the program – especially employers not using the funds to pay their employees. The government may be proposing anti-abuse rules and new criminal offences to ensure the subsidy is not inappropriately obtained. Penalties may include fines or imprisonment.

Does my business qualify?

The Canada Emergency Wage Subsidy applies to employers of all sizes. To be eligible, you must:

- be an employer who is an individual, taxable corporation, partnership consisting of eligible employers, non-profit organization, or registered charity; and

- experience a drop of at least 30% of your revenue in March, April or May, when compared to the same month in 2019.

You are not eligible if you are:

- a public body, including a municipality, local government, Crown corporation, public university, college, school or hospital.

Revenue for this purpose includes revenue from business carried on in Canada earned from arm’s-length sources. Revenue is calculated using your normal accounting method and excludes revenues from extraordinary items and amounts on account of capital. If your business was established after February 2019, monthly revenues will be compared to a reasonable benchmark.

The government is continuing to work with non-profits and charities to define revenue for their specific circumstances and is considering providing additional support to those involved in the front-line response to COVID-19.

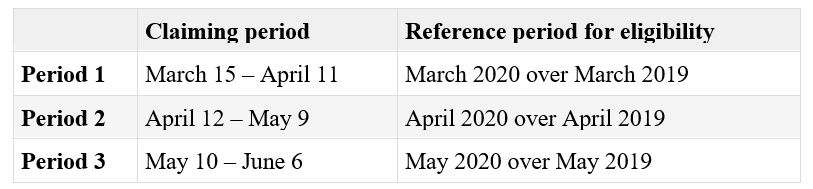

The funds you receive as wage subsidy are not counted for the purpose of measuring changes in monthly revenues. The government has provided the following table outlining each claiming period and the reference period in which a business has a decline in revenue of 30% or more.

How do I apply?

You will be able to apply through the Canada Revenue Agency’s My Business Account portal or a web-based application. Employers need to keep records showing their reduction in arm’s-length revenues and remuneration paid to employees.

The government will be providing further details about the application process shortly.

If my business does not qualify, can my business still apply to receive the 10% wage subsidy?

Yes. If your business is not eligible for the Canada Emergency Wage Subsidy, you may still qualify for the Temporary Wage Subsidy for Employers. This program allows employers to reduce the amount of payroll deductions to the Canada Revenue Agency from March 18, 2020 to June 19, 2020. The subsidy is equal to 10% of the remuneration you pay during that time, up to $1,375 for each eligible employee and up to a maximum of $25,000 total per employer.

You will be eligible for the 10% wage subsidy program if you:

- are a(n):

- individual (excluding trusts),

- partnership (if the members consist of individuals (excluding trusts), registered charities, or Canadian-controlled private corporations eligible for the small business deduction),

- non-profit organization,

- registered charity, or

- Canadian-controlled private corporation (including a cooperative corporation) eligible for the small business deduction;

- have an existing business number and payroll program account with the CRA on March 18, 2020; and

- pay salary, wages, bonuses, or other remuneration to an eligible employee, meaning an individual who is employed in Canada.

If you are eligible, you do not need to apply for the subsidy, but you will need to calculate the subsidy manually. The CRA will not automatically calculate it. Your subsidy calculation is based on the total number of eligible employees employed at any time during the three-month period.

As usual, you will continue to deduct income tax, Canada Pension Plan contributions, and Employment Insurance premiums from salary, wages, bonuses, or other remuneration paid to your employees. The subsidy is calculated when you remit these amounts to the CRA.

You can reduce your current payroll remittance of federal, provincial, or territorial income tax that you send to the CRA by the amount of the subsidy you calculate. You cannot reduce your remittance of CPP contributions or EI premiums.

The foregoing information provides only an overview of these subsidies as of the date this information has been provided. Specific legal advice should be obtained. If you have questions in the above regard, please contact the Head of our Business Law Group, Robert P. Kinghan, at (613) 566-2848 or rkinghan@perlaw.ca.